In an environment where inflation remains a concern, interest rates are closely watched after successive policy actions by the Reserve Bank of India, and household budgets are under pressure, avoiding unnecessary bank charges has become more important than ever.

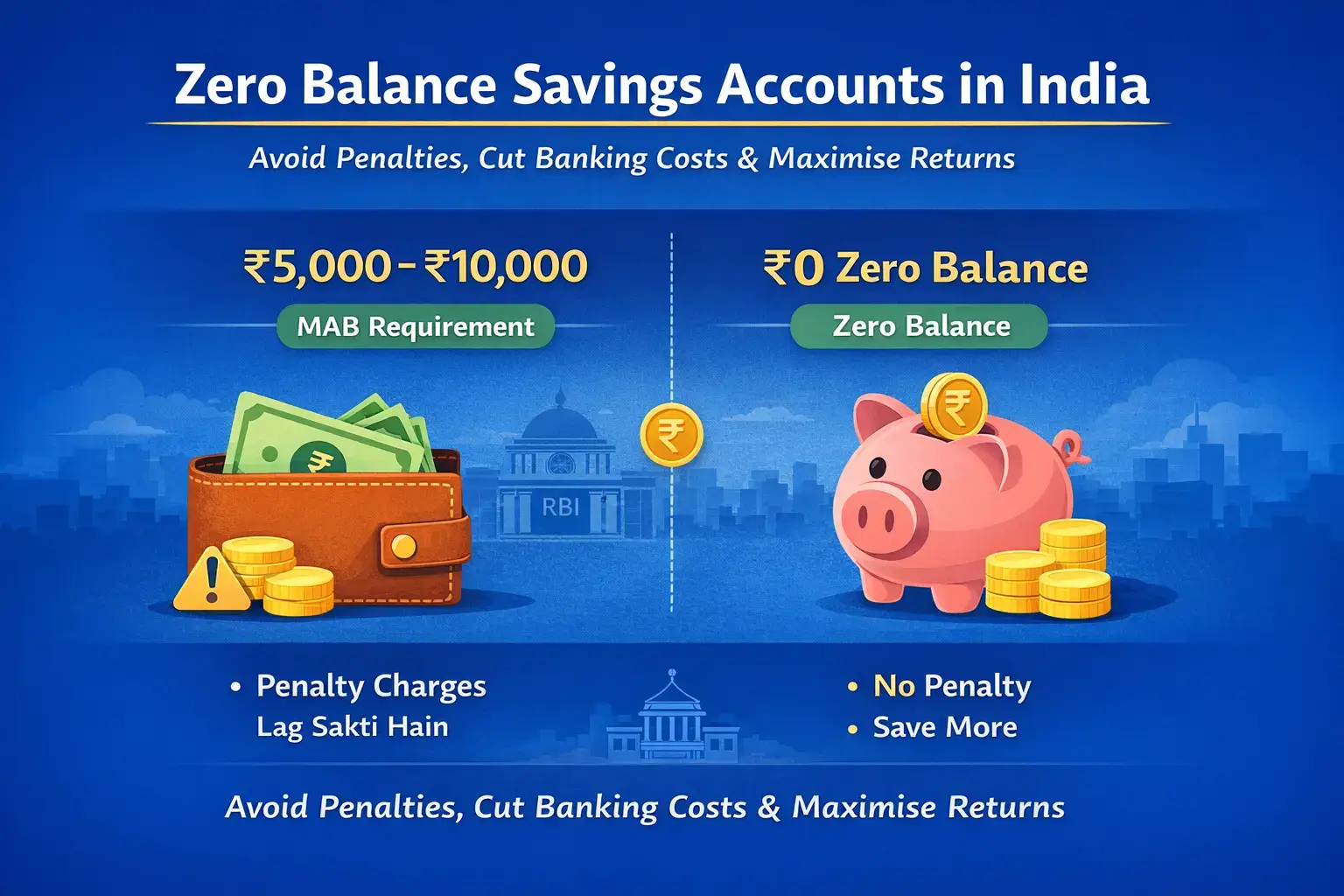

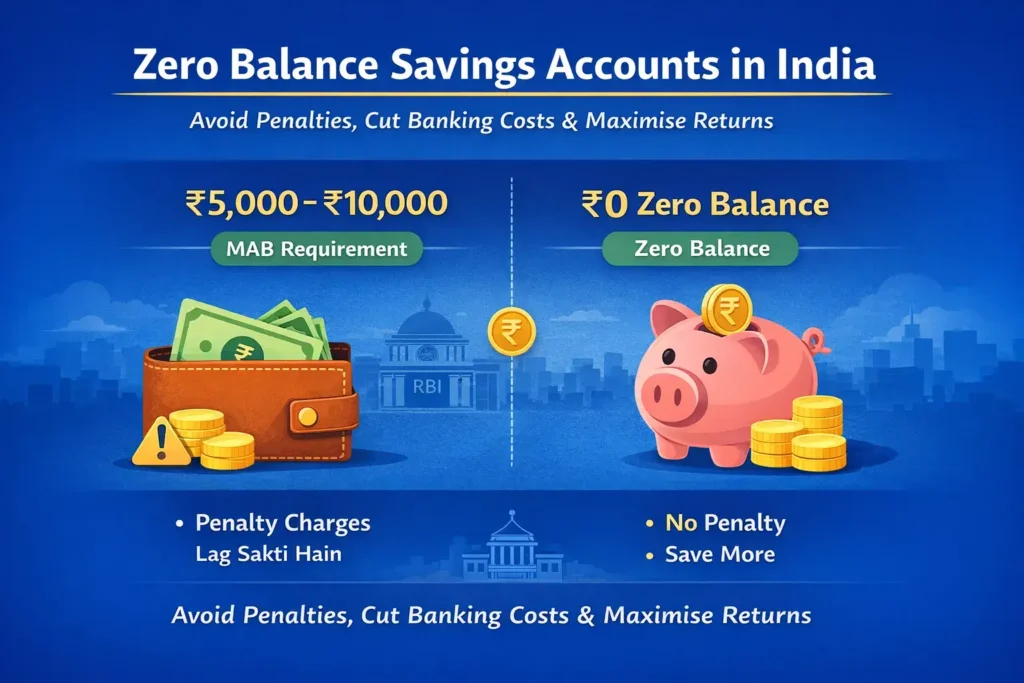

For millions of Indian consumers students, salaried employees, gig workers, small business owners, and retirees the Zero Balance Savings Account is emerging as a practical solution. Unlike traditional savings accounts that require maintaining a Monthly Average Balance (MAB), zero balance accounts eliminate penalty risks while offering essential banking services.

With rapid digital adoption, Video KYC onboarding, and tighter regulatory supervision by the RBI, Indian banks both private and public sector now offer multiple zero balance options. But are they truly free? What are the hidden costs? And which option suits your financial profile?

This detailed guide answers all these questions with a fact-based, regulation-backed analysis tailored for Indian readers.

Understanding Monthly Average Balance (MAB) and Why It Matters

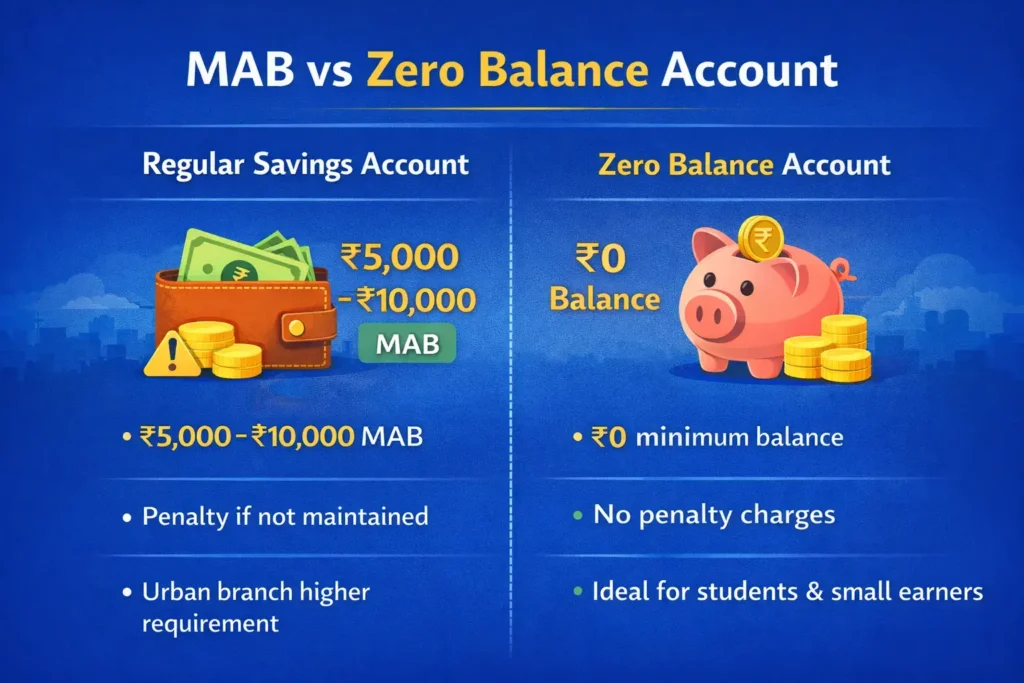

Most regular savings accounts in India require customers to maintain a Monthly Average Balance (MAB), typically ranging between ₹5,000 and ₹10,000 in urban branches. In metro cities, this requirement can be even higher.

If the balance falls below the threshold, banks impose non-maintenance penalties plus GST. Over a year, this can significantly erode savings especially for:

- Students

- Low-income earners

- First-time job holders

- Small traders and MSMEs

Zero balance accounts eliminate this requirement. Even if your account balance is ₹0, no penalty is charged subject to compliance with regulatory conditions.

Regulatory Background: RBI’s Framework for Zero Balance Accounts

The RBI permits banks to offer Basic Savings Bank Deposit Accounts (BSBDA) under financial inclusion norms. These accounts:

- Do not require minimum balance

- Allow basic ATM/debit card facility

- Offer limited free transactions (usually 4 withdrawals per month)

- Restrict multiple BSBDA accounts per individual

This initiative aligns with India’s broader financial inclusion push under schemes like Jan Dhan Yojana and digital banking reforms.

However, RBI also allows banks to design digital savings accounts with zero MAB, subject to full KYC compliance.

Understanding this regulatory distinction is important before choosing an account.

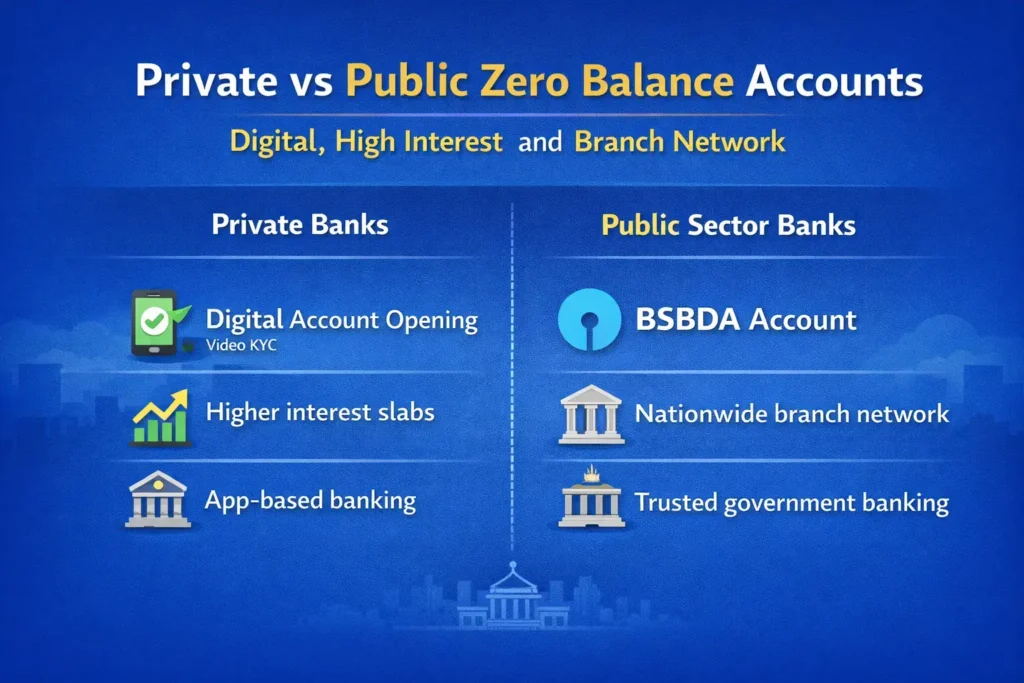

Private Sector Zero Balance Accounts: Digital Convenience vs Conditions

Private banks have aggressively promoted digital zero balance accounts. Let’s examine the most discussed options.

1. Kotak Mahindra Bank – Kotak 811 Digital Account

Kotak 811 is one of India’s most popular fully digital zero balance accounts.

Key Features:

- Zero MAB requirement

- Fully digital onboarding via Video KYC

- Virtual debit card (physical card optional)

- UPI, net banking, mobile banking

Why It Appeals:

- No mandatory maintenance charges

- Quick account opening (often within minutes)

- Suitable for young earners and digital-first users

Things to Check:

- Physical debit card annual fee

- Transaction limits before full KYC

- Upgrade requirements for higher balances

For salaried professionals comfortable with online banking, Kotak 811 offers a seamless experience.

2. AU Small Finance Bank – High Interest with Monthly Payout

AU Small Finance Bank stands out for offering comparatively higher interest rates (subject to slabs and policy changes).

Highlights:

- Zero balance digital account options

- Competitive savings interest rates

- Monthly interest credit (in eligible variants)

For customers parking idle funds while maintaining liquidity, higher interest rates can partially offset inflation impact.

However, always verify:

- Applicable balance slabs

- Debit card charges

- SMS alert fees

Interest rates are subject to revision based on RBI policy rates and liquidity conditions.

3. IndusInd Bank – Zero Balance with Initial Funding Conditions

IndusInd offers digital account variants marketed as zero balance accounts. However:

- Some variants may require initial funding

- Charges may apply based on product type

Always read the schedule of charges before opening.

4. HDFC Bank & ICICI Bank – Limited Zero Balance Options

India’s largest private banks typically require MAB in regular savings accounts.

True zero balance accounts are usually offered under:

- BSBDA category

- Salary account tie-ups

- Special schemes

These may include:

- Transaction limits

- Restricted cheque book issuance

For customers wanting premium features without maintaining balance, these banks may not be ideal unless eligibility criteria are met.

Public Sector Banks: Trust, Reach, and True Zero Balance

Public sector banks remain the backbone of Indian banking.

State Bank of India – Basic Savings Bank Deposit Account (BSBDA)

SBI’s BSBDA is one of the most widely used zero balance accounts in India.

Key Benefits:

- No minimum balance requirement

- Nationwide branch network

- RuPay debit card facility

- Basic digital banking

Limitations:

- Only 4 free withdrawals per month

- No frills account structure

- Restrictions on additional facilities

For rural and semi-urban customers, SBI’s reach provides unmatched accessibility.

Bank of Baroda & India Post Payments Bank

These institutions offer reliable zero balance or low-balance banking options.

India Post Payments Bank especially serves remote regions where traditional bank access is limited.

They are ideal for:

- Senior citizens

- Pensioners

- Individuals preferring physical banking

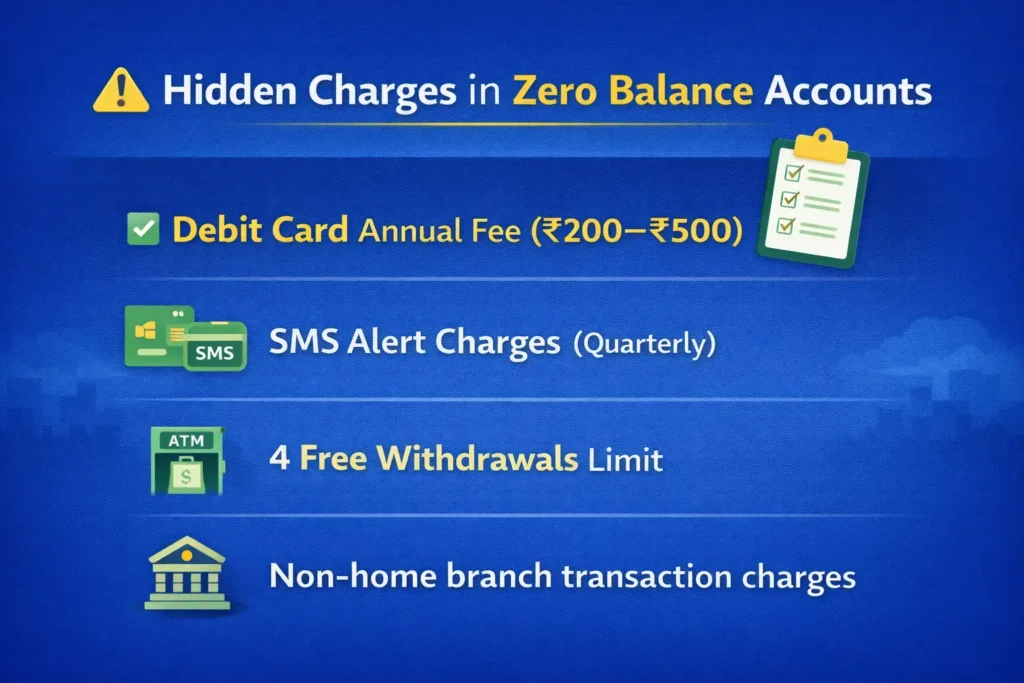

Hidden Charges: What Most Indians Overlook

Zero balance does not always mean zero cost.

Before opening an account, carefully review:

1. Debit Card Annual Fee

Typically ranges between ₹200 to ₹500 plus GST.

2. SMS Alert Charges

Banks may charge ₹15–₹30 per quarter.

3. ATM Withdrawal Limits

BSBDA accounts usually allow only 4 free withdrawals per month (including ATM).

4. Non-Home Branch Transactions

Some banks charge for over-the-counter transactions beyond limits.

Reading the official Schedule of Charges available on bank websites is essential.

Digital Account Opening: Video KYC and Documentation

Most major banks now offer Video KYC-based account opening.

Required Documents:

- Original PAN Card

- Aadhaar Card (linked with mobile number)

- Active mobile number

The process generally includes:

- Live video verification

- PAN validation

- Signature capture

This digital transformation aligns with RBI’s push toward paperless banking and financial inclusion.

Impact on Everyday Indians

Zero balance accounts influence financial planning in several ways:

1. Income Tax & Cash Flow Management

With the new vs old tax regime choices, salaried individuals need liquidity to manage tax-saving investments like PPF, ELSS SIPs, and NPS contributions. Avoiding penalty charges helps preserve investible surplus.

2. Credit Score (CIBIL) Stability

While savings accounts do not directly affect CIBIL scores, bounced ECS payments due to insufficient funds can indirectly damage credit history.

3. SIP and Investment Discipline

Many investors link SIP mandates to savings accounts. Zero balance flexibility reduces stress of maintaining minimum thresholds while investing regularly.

4. Small Business & MSME Utility

For freelancers and micro-businesses managing fluctuating cash flows, zero balance accounts prevent penalty during lean months.

Risks and Practical Limitations

While beneficial, zero balance accounts have constraints:

- Limited transaction count

- Lower priority customer service in basic variants

- Fewer premium features

- Restrictions on multiple accounts

Customers requiring frequent high-value transactions may find regular accounts more suitable.

Expert Perspective: When Should You Choose Zero Balance?

Choose a zero balance account if:

- You are a student or first-time job holder

- Your income is irregular

- You want a secondary account for UPI and digital payments

- You prefer avoiding MAB penalties

Avoid if:

- You maintain high balances consistently

- You require unlimited branch transactions

- You want premium debit cards or concierge services

Future Outlook: Digital Banking and Financial Inclusion

India’s banking sector continues to evolve under RBI supervision, fintech integration, and regulatory oversight.

With:

- Expanding UPI ecosystem

- Digital KYC frameworks

- Increased rural banking penetration

Zero balance accounts will likely grow further especially among Gen Z, gig economy workers, and rural entrepreneurs.

However, customers must remain informed and compare features carefully.

Final Verdict: Which Bank Should You Choose?

- For fully digital experience: Kotak 811 or AU Small Finance Bank

- For high interest (subject to slabs): AU Bank

- For trust and branch reach: SBI BSBDA

- For traditional banking preference: Bank of Baroda or India Post

There is no single “best” bank. The right choice depends on your income pattern, digital comfort level, transaction frequency, and financial goals.

In 2026, when cost efficiency and liquidity matter more than ever, zero balance savings accounts offer a smart way to eliminate unnecessary penalties while staying financially flexible.

But smart banking is not about avoiding balance requirements alone it is about understanding charges, regulations, transaction limits, and aligning your account choice with your broader financial strategy.

Before opening any account, read official documentation, verify charges from bank websites, and ensure the product fits your long-term financial planning goals.

Financial awareness not marketing claims is your strongest asset.

What is a Zero Balance Savings Account in India?

A Zero Balance Savings Account is a bank account where you are not required to maintain a Monthly Average Balance (MAB). Unlike regular savings accounts that require ₹5,000–₹10,000 minimum balance (depending on city category), these accounts do not charge penalty even if your balance is ₹0.

Most zero balance accounts are offered under RBI’s Basic Savings Bank Deposit Account (BSBDA) framework.

Is Zero Balance Account really free?

Yes, but partially.

While there is:

No minimum balance requirement

No MAB penalty

Banks may still charge:

Debit card annual fee (₹200–₹500)

SMS alert charges

Charges after exceeding free transaction limits

Always check the bank’s official schedule of charges before opening an account.

Which bank is best for Zero Balance Account in India?

It depends on your needs:

For strong branch network and trust:

State Bank of India (BSBDA account)

For digital experience:

Kotak Mahindra Bank (Kotak 811)

For higher interest rates:

AU Small Finance Bank

For premium digital banking:

IndusInd Bank

Choose based on interest rate, branch access, and digital features.

What is BSBDA Account?

BSBDA stands for Basic Savings Bank Deposit Account. It is a zero balance account category introduced under guidelines of the Reserve Bank of India.

Key features:

Zero minimum balance

4 free withdrawals per month

ATM-cum-debit card facility

Basic banking services

It is mainly designed for financial inclusion.

Can I open a Zero Balance Account online?

Yes.

Most banks now allow online account opening through:

Video KYC

Aadhaar-based verification

PAN authentication

Banks like Kotak Mahindra Bank, AU Small Finance Bank, and State Bank of India offer digital account opening.

How many free transactions are allowed in Zero Balance Accounts?

In most BSBDA accounts:

Only 4 free withdrawals per month (including ATM withdrawals)

After that, charges may apply

Private digital zero balance accounts may have slightly different limits. Always verify before applying.

Does Zero Balance Account affect CIBIL score?

No.

Opening or maintaining a zero balance savings account does not impact your CIBIL score because:

It is not a credit product

There is no borrowing involved

Your CIBIL score is affected only by loans, credit cards, and repayment behavior.

What documents are required to open a Zero Balance Account?

Generally required documents include:

PAN Card

Aadhaar Card (linked with mobile number)

Active mobile number

Passport-size photograph (for branch opening)

For digital accounts, Video KYC is mandatory.

Can I convert my regular savings account into Zero Balance Account?

Yes, in some cases.

You may request your bank to convert it into a BSBDA account, subject to eligibility and internal bank policy. However, you cannot hold both a regular savings account and a BSBDA account in the same bank simultaneously.

Sachin is a professional blogger who believes in “Human-First” content. He specializes in breaking down complicated tech and finance topics into simple, actionable steps. His goal is to empower users with the right knowledge to make smarter digital decisions.