Your CIBIL score quietly decides a lot about your financial life. Whether you’re applying for a credit card, a personal loan, or even negotiating interest rates, this three-digit number plays a major role.

If your score is low, it can feel frustrating. Applications get rejected, offers look unattractive, and suddenly everything becomes harder than it should be. The good news? A poor credit score is not permanent. With the right approach, you can rebuild it step by step.

This guide will walk you through how to improve your CIBIL score, using practical strategies that actually work in real life, not just theory.

What is a CIBIL Score and Why It Matters

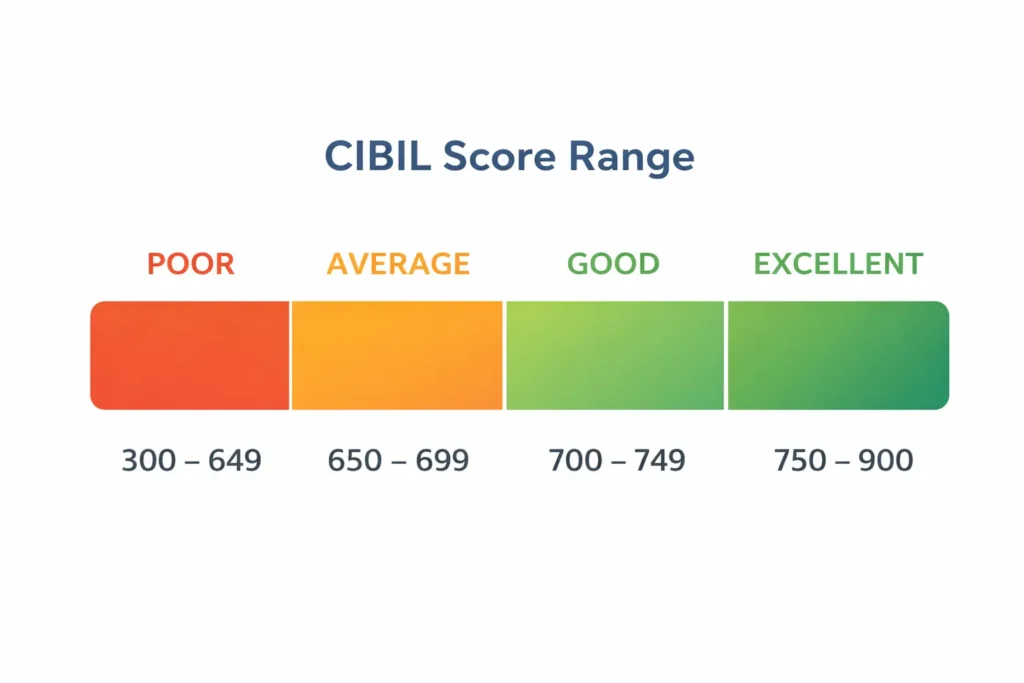

A CIBIL score is a three-digit number ranging from 300 to 900, calculated based on your credit history. It reflects your creditworthiness, which simply means how reliable you are at repaying borrowed money.

- 750 and above – Strong profile, high approval chances

- 650 to 749 – Decent, but not ideal

- Below 650 – Risky for lenders

Banks and NBFCs use this score to evaluate:

- Loan eligibility

- Interest rates

- Credit card limits

According to TransUnion CIBIL, payment behaviour and credit usage are the biggest factors influencing your score. This means your daily financial habits matter more than anything else.

What Impacts Your CIBIL Score (Deep Understanding)

Before fixing your score, you need to understand what actually affects it.

1. Payment History

This is the most critical factor. Missing even a single EMI or credit card payment can negatively impact your score.

Timely payments signal financial discipline, while delays increase your risk profile.

2. Credit Utilisation Ratio

This refers to how much credit you’re using compared to your total limit.

Example:

If your limit is ₹1,00,000 and you use ₹80,000, your utilisation is 80% which is high.

Experts generally recommend keeping it below 30% to maintain a healthy credit profile.

3. Length of Credit History

A longer credit history builds trust. Lenders prefer borrowers who have handled credit responsibly over time.

4. Credit Mix

Having a balance of:

- Secured loans (home loan, car loan)

- Unsecured credit (credit cards, personal loans)

This improves your overall credit profile.

5. Hard Inquiries

Each loan or credit card application creates a “hard inquiry.” Too many inquiries in a short period can lower your score.

Common Reasons for a Poor CIBIL Score

In most cases, a low score isn’t caused by one big mistake, it’s a combination of small habits:

- Missing EMI or credit card due dates

- Paying only the minimum due

- Using a high percentage of your credit limit

- Settling loans instead of closing them properly

- Applying for multiple loans within a short time

- Ignoring errors in your credit report

These behaviours signal poor debt management, which reduces lender confidence.

How to Improve CIBIL Score (Step-by-Step Strategy)

Now let’s focus on what actually works.

1. Pay All EMIs and Bills on Time

This is non-negotiable. Your repayment history directly affects your score.

Set up:

- Auto-debit instructions

- Payment reminders

- Calendar alerts

Even a 30-day delay can stay in your report for years.

2. Reduce Your Credit Utilisation Ratio

If you’re regularly using more than 50–60% of your credit limit, it’s time to cut back.

Practical tips:

- Spread expenses across multiple cards

- Request a credit limit increase

- Avoid unnecessary large purchases on credit

This simple change can significantly improve your score over time.

3. Avoid Frequent Loan Applications

Every application creates a hard inquiry. Too many inquiries suggest credit dependency.

Instead:

- Check eligibility before applying

- Space out applications by at least 3–6 months

This protects your credit profile from unnecessary damage.

4. Don’t Close Old Credit Cards

Old accounts increase your credit history length.

Even if you don’t actively use a card:

- Keep it active with small transactions

- Pay the balance in full

Closing old accounts can reduce your overall credit age and hurt your score.

5. Clear Outstanding Dues Properly

If you have unpaid loans or credit card balances, prioritise clearing them.

Important:

Avoid “settlements” whenever possible. A settled account is viewed negatively by lenders.

Always aim for full repayment, even if it takes time.

6. Check and Correct Credit Report Errors

Errors in your credit report are more common than people think.

You should regularly review your report for:

- Incorrect late payments

- Duplicate accounts

- Loans you never took

If you find an issue, raise a dispute with CIBIL. Fixing errors can sometimes improve your score quickly.

(You can check your report through official platforms like TransUnion CIBIL or RBI-authorised services.)

7. Build or Rebuild Your Credit Profile

If your score is very low or you have no credit history:

Start small:

- Use a secured credit card against a fixed deposit

- Take a small loan and repay on time

This creates a positive repayment track record and improves your financial credibility.

How to Increase CIBIL Score from 600 to 750

Moving from 600 to 750 is absolutely achievable, but it requires consistency.

Here’s a realistic approach:

- Month 1–2: Clear dues and stop late payments

- Month 3–4: Reduce credit utilisation below 30%

- Month 5–6: Maintain perfect payment behaviour

- Month 6+: Avoid new credit unless necessary

Over time, your improved repayment behaviour strengthens your creditworthiness.

How Long Does It Take to Improve Your Credit Score?

Improvement doesn’t happen overnight.

- Short-term (1–3 months): Small improvements

- Medium-term (3–6 months): Noticeable changes

- Long-term (6–12 months): Strong recovery

According to industry observations, consistent behaviour matters more than quick fixes.

Common Mistakes That Keep Your Score Low

Even after trying to improve, many people unknowingly repeat these mistakes:

- Paying only the minimum due on credit cards

- Ignoring small overdue amounts

- Closing old credit accounts

- Frequently switching lenders

- Not tracking their credit report

These habits slow down your progress.

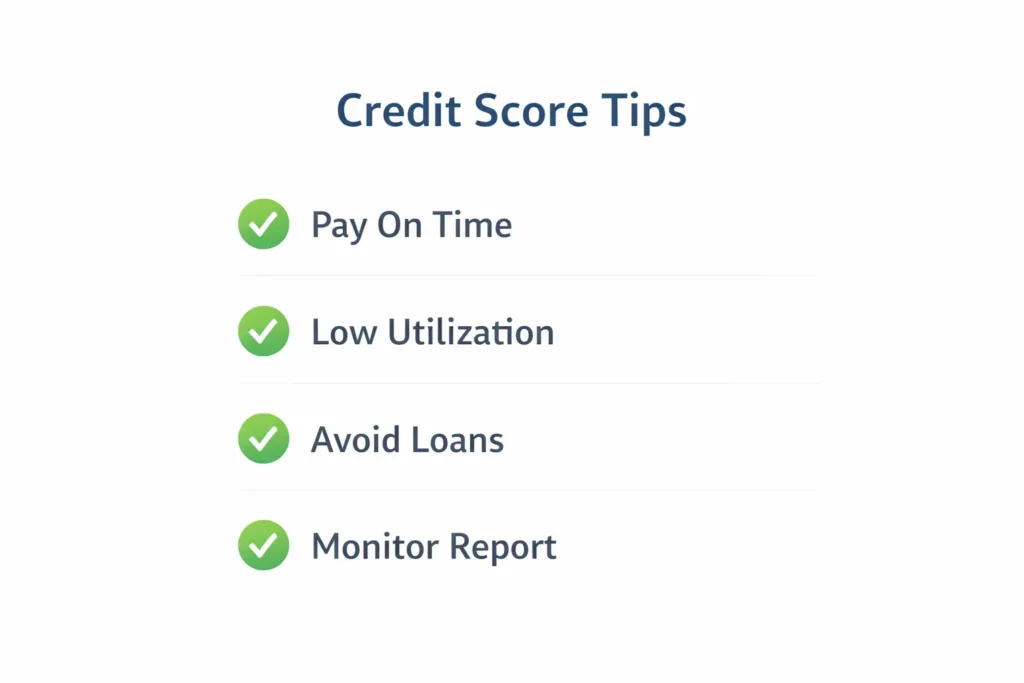

Expert Tips to Maintain a Good CIBIL Score

Once your score improves, maintaining it is equally important.

- Always pay the full credit card bill

- Keep utilisation low, even if your limit increases

- Avoid unnecessary loans

- Monitor your credit report at least twice a year

- Maintain a healthy mix of credit

Think of your credit score as a long-term asset not something to fix once and forget.

Real-Life Example (Practical Insight)

Consider this simple case:

A borrower had:

- Score: 590

- High credit usage

- Multiple missed payments

Instead of rushing into new loans, they focused on:

- Clearing dues

- Reducing usage to 25%

- Maintaining on-time payments

Within 6–8 months, the score improved significantly, crossing 700.

The takeaway? There’s no shortcut, but there is a clear path.

Final Thoughts

Improving your CIBIL score is less about tricks and more about consistent financial behaviour.

Focus on:

- Timely repayments

- Smart credit usage

- Responsible borrowing

Over time, your credit profile strengthens naturally, improving your loan eligibility and financial flexibility.

How can I improve my CIBIL score quickly?

You can improve your CIBIL score by paying all EMIs and credit card bills on time, keeping your credit utilization below 30%, and avoiding frequent loan applications. Small but consistent actions can show improvement within a few months.

How long does it take to improve a CIBIL score?

Improving a CIBIL score usually takes 3 to 6 months for noticeable changes and up to 12 months for strong improvement. The timeline depends on your repayment history and credit behaviour.

Can I increase my CIBIL score from 600 to 750?

Yes, it is possible to increase your CIBIL score from 600 to 750 by maintaining timely payments, reducing credit usage, and avoiding loan settlements. Consistency is the key to long-term improvement.

What is the minimum CIBIL score required for loan approval?

Most banks in India prefer a CIBIL score of 700 or above for easy loan approval. However, some lenders may approve loans at lower scores with higher interest rates.

Does checking my CIBIL score reduce it?

No, checking your own CIBIL score is considered a soft inquiry and does not affect your score. Only lender checks (hard inquiries) impact your score.

How to improve CIBIL score after late payment?

To improve your score after a late payment, ensure all future payments are on time, clear any outstanding dues, and maintain low credit utilization. Over time, the impact of late payments reduces.

Is loan settlement bad for CIBIL score?

Yes, loan settlement negatively impacts your CIBIL score because it shows that you did not fully repay your loan. Always try to close loans completely instead of settling them.

What is a good credit utilisation ratio?

A good credit utilization ratio is below 30% of your total credit limit. Lower usage indicates better financial discipline and improves your credit score.

Can I improve my CIBIL score without a credit card?

Yes, you can improve your score by taking a small loan and repaying it on time or using a secured credit card against a fixed deposit.

Why is my CIBIL score not increasing even after paying on time?

Your score may not increase due to high credit utilization, multiple loan inquiries, or past negative records like settlements. Improving your overall credit behavior will gradually increase your score.

Sachin is a professional blogger who believes in “Human-First” content. He specializes in breaking down complicated tech and finance topics into simple, actionable steps. His goal is to empower users with the right knowledge to make smarter digital decisions.