Most investors obsess over where to earn the highest returns.

Fewer think about where to park money safely while waiting.

That gap in thinking quietly costs money.

If you keep surplus cash in a savings account earning 2-3%, or idle in a trading account doing nothing, you’re sacrificing opportunity. This is where liquid ETFs can help.

In this guide, we’ll explain:

- What liquid ETFs are

- How they work

- How they compare with fixed deposits

- Risks involved

- How to evaluate the best liquid ETFs in India

- Who should use them (and who shouldn’t)

This article follows verified regulatory definitions and publicly available data from trusted sources like the Securities and Exchange Board of India (SEBI), Reserve Bank of India (RBI), and AMFI (Association of Mutual Funds in India).

Let’s begin with clarity.

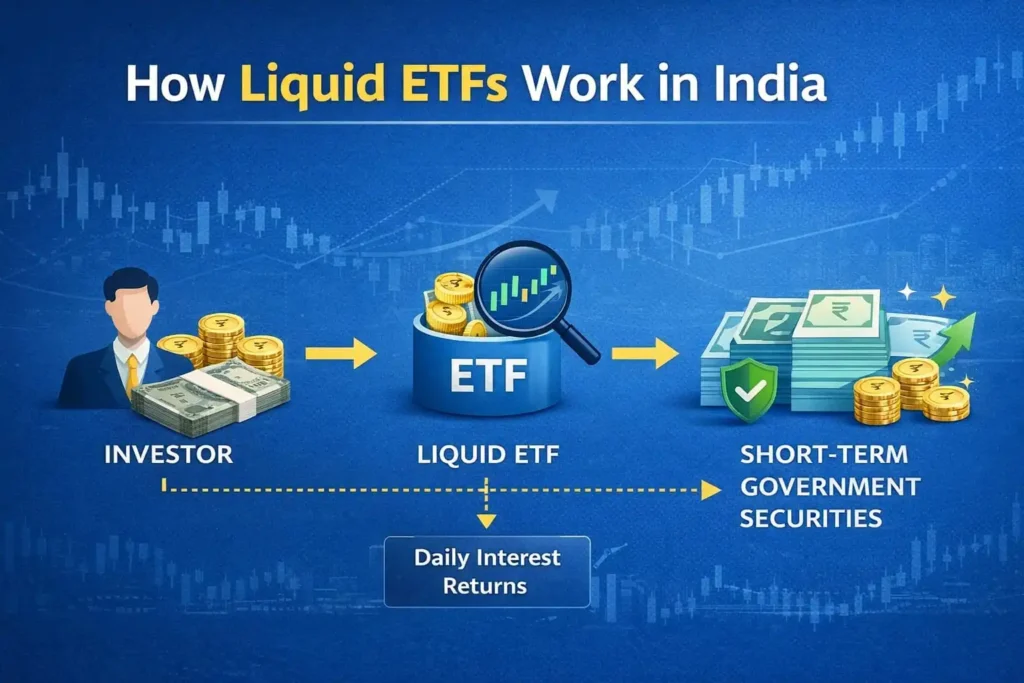

What Is a Liquid ETF?

A Liquid ETF (Exchange-Traded Fund) is a debt-based ETF that invests in very short-term money market instruments.

These typically include:

- Treasury Bills (T-Bills) issued by the Government of India

- Reverse repo and overnight instruments

- Short-duration money market securities

SEBI classifies liquid funds as those investing in debt and money market securities with maturity up to 91 days (SEBI Mutual Fund Regulations). Liquid ETFs follow a similar short-duration structure but trade on stock exchanges like shares.

Unlike traditional liquid mutual funds, liquid ETFs:

- Trade in real time on stock exchanges

- Require a demat and trading account

- Allow buying and selling during market hours

In simple terms, a liquid ETF acts as a low-risk parking space for short-term capital.

Why Are Liquid ETFs Relevant in India Today?

India’s monetary policy is governed by the Reserve Bank of India (RBI). When the RBI adjusts the repo rate, short-term money market yields respond.

As per RBI monetary policy data, short-term instruments often reflect prevailing interest rates more quickly than long-term bonds.

Savings accounts in India generally offer around 2.5%–4% annually (varies by bank). Fixed deposits offer higher rates depending on tenure and bank policy.

Liquid ETFs typically aim to reflect overnight or short-term money market yields. These yields fluctuate based on RBI policy but have historically been higher than basic savings account rates.

This is why many investors research:

“Best liquid ETFs in India”

They are not chasing aggressive returns.

They are optimizing idle capital.

How Liquid ETFs Generate Returns

Liquid ETFs earn income primarily from:

1. Interest income from underlying securities

2. Compounding of short-term yields

3. Efficient portfolio rollover

Because these instruments mature quickly, interest rate sensitivity remains low compared to long-duration bond funds.

When rates rise, liquid instruments reset faster.

When rates fall, yields adjust accordingly.

This makes liquid ETFs relatively stable compared to equity investments.

They are designed for:

- Capital preservation

- High liquidity

- Moderate, short-term returns

Not wealth multiplication.

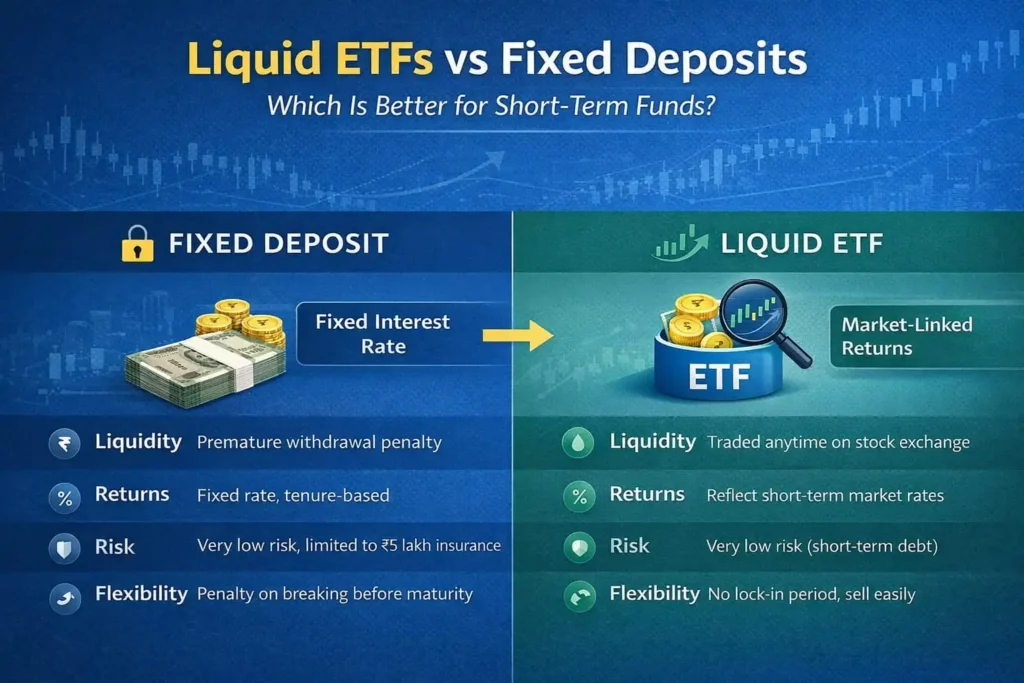

Liquid ETFs vs Fixed Deposits: A Clear Comparison

Investors often compare liquid ETFs with fixed deposits (FDs). Let’s examine the differences objectively.

1. Returns

Fixed Deposit (FD):

- Interest rate fixed at booking

- Rates vary by tenure and bank

- Public data available on RBI and bank websites

Liquid ETF:

- Market-linked short-term yield

- Not fixed in advance

- Reflects money market conditions

FDs provide certainty.

Liquid ETFs provide flexibility.

2. Liquidity

Fixed Deposit:

- Premature withdrawal penalty

- Interest recalculated on early closure

Liquid ETF:

- Sell anytime during market hours

- Settlement as per exchange rules (currently T+1 for many segments as per SEBI circulars)

Liquid ETFs clearly offer superior flexibility.

3. Risk Profile

Fixed Deposit:

- Considered low risk

- Deposit insurance up to ₹5 lakh per bank per depositor under DICGC (RBI-regulated)

Liquid ETF:

- Invests in short-term instruments

- Subject to minimal market fluctuation

- Not covered by deposit insurance

Both are low-risk.

FDs offer insurance protection within limits.

Liquid ETFs depend on portfolio quality.

4. Taxation

Taxation rules change over time and investors should check current regulations.

- FD interest is taxed as per your income slab.

- Debt ETF capital gains taxation depends on holding period and prevailing tax law.

Refer to Income Tax Department guidelines or consult a qualified advisor before making decisions.

Who Should Consider Liquid ETFs?

Liquid ETFs may suit:

1. Active Traders

Traders often keep unused margin capital. Instead of leaving it idle, liquid ETFs allow capital efficiency.

2. Investors Waiting for Market Corrections

If you are waiting for better entry points, parking funds in liquid ETFs can be more efficient than savings accounts.

3. Business Owners

Short-term surplus cash can remain productive while staying accessible.

4. Emergency Fund Allocation (Partial)

Some investors allocate a portion of emergency funds to liquid ETFs while keeping immediate cash in savings accounts.

Who Should Avoid Liquid ETFs?

Liquid ETFs are not ideal for:

- Long-term wealth creation

- High-return expectations

- Beating inflation significantly

- Replacing equity allocation

They are a cash-management tool.

Risks You Must Understand

Even low-risk instruments carry some risk.

1. Market Price Variation

Since ETFs trade on exchanges, price may slightly differ from NAV.

2. Liquidity Risk

Low trading volume can impact execution price.

3. Credit Risk

Although rare in high-quality portfolios, debt instruments carry credit exposure.

Investors should review:

- Portfolio quality

- AMC track record

- Fund disclosures

All mutual fund and ETF disclosures are available on AMFI and AMC websites.

How to Choose the Best Liquid ETFs in India

Instead of chasing “top returns,” focus on structure and quality.

1. Expense Ratio

Lower expense ratio means better net yield retention.

2. Assets Under Management (AUM)

Larger AUM often indicates better liquidity and investor confidence.

3. Trading Volume

Check average daily traded quantity on exchange.

4. Portfolio Quality

Review portfolio disclosure from AMC website.

5. Tracking Efficiency

Compare ETF performance with benchmark index.

Well-known liquid ETFs in India include offerings from established AMCs such as:

- Nippon India

- ICICI Prudential

- HDFC

- SBI

- Kotak

Investors must review latest data before investing.

Practical Example: Capital Efficiency Matters

Imagine you hold ₹10 lakh in cash for 6 months while waiting for a market opportunity.

If parked in a low-interest savings account, returns remain modest.

If placed in a liquid ETF aligned with short-term money market yields, returns may improve — depending on prevailing rates.

Over years, this difference compounds.

Liquid ETFs won’t transform your wealth overnight.

But efficient capital allocation compounds quietly.

And finance rewards discipline.

The Mindset Shift: Stop Letting Money Sleep

Smart investing is not only about high returns.

It is about:

- Reducing inefficiency

- Improving capital utilization

- Managing liquidity wisely

Liquid ETFs solve a simple problem:

“What should I do with short-term idle funds?”

That question matters more than most investors realize.

Final Thoughts: Should You Invest?

If you regularly have money:

- Waiting for deployment

- Sitting in trading accounts

- Temporarily unused

Then exploring the best liquid ETFs in India makes strategic sense.

They are not exciting.

They are not aggressive.

They are not viral on social media.

They are simply efficient.

And efficient capital management builds long-term financial strength.

Before investing, review fund documents carefully and consult a registered financial advisor if needed. Always align investments with your financial goals and risk tolerance.

Because in investing, small disciplined decisions often outperform dramatic ones.

If you want next-level optimization, I can now provide:

- SEO meta title + description aligned to Google CTR data

- Internal linking strategy for finance blog

- Schema-ready FAQ markup

- WordPress-ready formatting structure

- Or a content cluster strategy around “Short-Term Investments in India”

Frequently Asked Questions (FAQ)

1. What is a Liquid ETF in India?

A Liquid ETF is an exchange-traded fund that invests in short-term debt instruments such as treasury bills, government securities, and high-quality money market instruments. It is designed to park surplus cash while maintaining high liquidity and relatively low risk.

2. Are Liquid ETFs safer than Fixed Deposits?

Liquid ETFs and Fixed Deposits serve different purposes. Fixed Deposits offer guaranteed returns backed by banks, while Liquid ETFs invest in short-term debt instruments and carry low but market-linked risk. They are generally considered low-risk, but returns are not guaranteed.

3. How are Liquid ETFs taxed in India?

Liquid ETFs are taxed as debt mutual funds. Capital gains tax depends on your holding period and current tax rules. Investors should check the latest taxation guidelines or consult a tax advisor, as regulations may change.

4. Can I lose money in a Liquid ETF?

While Liquid ETFs are considered low-risk, they are not risk-free. Interest rate movements and credit risk can cause small fluctuations in returns. However, they are generally more stable compared to equity investments.

5. How quickly can I withdraw money from a Liquid ETF?

Since Liquid ETFs are traded on stock exchanges, you can sell them during market hours. Settlement typically happens as per exchange norms (T+1 or applicable cycle).

6. Who should invest in Liquid ETFs?

Liquid ETFs are suitable for:

Investors parking short-term surplus funds

Emergency fund allocation

Businesses managing working capital

Investors seeking slightly better flexibility than traditional deposits

7. What should I check before investing in a Liquid ETF?

Key factors include:

Expense ratio

AUM (Assets Under Management)

Portfolio quality

Liquidity and trading volume

Reputation of the fund house

Sachin is a professional blogger who believes in “Human-First” content. He specializes in breaking down complicated tech and finance topics into simple, actionable steps. His goal is to empower users with the right knowledge to make smarter digital decisions.